All Categories

Featured

[/image][=video]

[/video]

Withdrawals from the cash money value of an IUL are usually tax-free as much as the amount of costs paid. Any withdrawals above this amount may be subject to tax obligations depending on policy framework. Standard 401(k) payments are made with pre-tax bucks, reducing gross income in the year of the payment. Roth 401(k) payments (a plan function readily available in a lot of 401(k) plans) are made with after-tax contributions and afterwards can be accessed (earnings and all) tax-free in retired life.

Withdrawals from a Roth 401(k) are tax-free if the account has been open for at the very least 5 years and the individual mores than 59. Possessions taken out from a typical or Roth 401(k) prior to age 59 might incur a 10% charge. Not specifically The cases that IULs can be your own bank are an oversimplification and can be misleading for several reasons.

You may be subject to updating connected health and wellness concerns that can affect your ongoing prices. With a 401(k), the money is always yours, consisting of vested employer matching regardless of whether you quit adding. Risk and Warranties: Firstly, IUL policies, and the cash money value, are not FDIC guaranteed like conventional checking account.

While there is typically a flooring to stop losses, the development capacity is covered (suggesting you may not totally take advantage of market upswings). The majority of professionals will certainly agree that these are not comparable products. If you want fatality benefits for your survivor and are concerned your retirement cost savings will certainly not be sufficient, after that you may intend to take into consideration an IUL or other life insurance coverage product.

Sure, the IUL can supply accessibility to a cash money account, yet once again this is not the main purpose of the product. Whether you desire or need an IUL is a highly private question and depends upon your main monetary goal and goals. Nonetheless, listed below we will try to cover benefits and constraints for an IUL and a 401(k), so you can further mark these products and make a more educated decision concerning the best way to handle retirement and taking care of your enjoyed ones after fatality.

Index Universal Life Insurance Companies

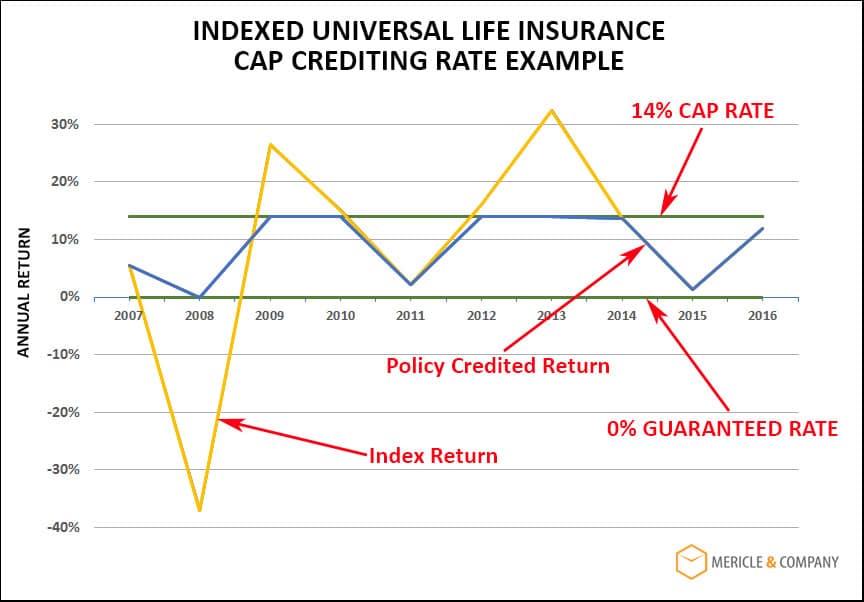

Funding Costs: Fundings versus the plan accrue passion and, if not settled, decrease the survivor benefit that is paid to the beneficiary. Market Engagement Restrictions: For a lot of plans, investment development is linked to a stock exchange index, however gains are generally topped, limiting upside possible - nationwide indexed universal life accumulator ii. Sales Practices: These policies are usually offered by insurance coverage representatives who might emphasize benefits without completely clarifying costs and risks

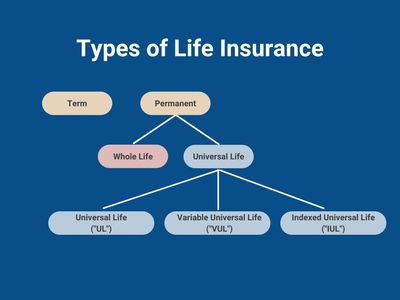

While some social media experts suggest an IUL is a replacement item for a 401(k), it is not. Indexed Universal Life (IUL) is a kind of permanent life insurance coverage policy that likewise offers a cash money value part.

{kind=link}

Latest Posts

Iul Companies

Indexed Universal Life Insurance

Index Universal Life Insurance Fidelity